Bitcoin

Bitcoin  Ethereum

Ethereum  Tether

Tether  XRP

XRP  BNB

BNB  Solana

Solana  Dogecoin

Dogecoin  USDC

USDC  Cardano

Cardano  Avalanche

Avalanche  Wrapped stETH

Wrapped stETH  Toncoin

Toncoin  Sui

Sui  Shiba Inu

Shiba Inu  Wrapped Bitcoin

Wrapped Bitcoin  Stellar

Stellar  Polkadot

Polkadot  Hyperliquid

Hyperliquid  Hedera

Hedera  WETH

WETH  Bitcoin Cash

Bitcoin Cash  LEO Token

LEO Token  Pepe

Pepe  Litecoin

Litecoin  Wrapped eETH

Wrapped eETH  NEAR Protocol

NEAR Protocol  Ethena USDe

Ethena USDe  Aptos

Aptos  USDS

USDS  Aave

Aave  POL (ex-MATIC)

POL (ex-MATIC)  Render

Render  MANTRA

MANTRA  Bittensor

Bittensor  WhiteBIT Coin

WhiteBIT Coin  Artificial Superintelligence Alliance

Artificial Superintelligence Alliance  Ethena

Ethena  Arbitrum

Arbitrum  Filecoin

Filecoin  Fantom

Fantom  Algorand

Algorand  OKB

OKB  Cosmos Hub

Cosmos Hub  Virtuals Protocol

Virtuals Protocol  Ondo

Ondo  Optimism

Optimism  Bonk

Bonk  Immutable

Immutable  Celestia

Celestia  Movement

Movement  Injective

Injective  The Graph

The Graph  dogwifhat

dogwifhat  Binance-Peg WETH

Binance-Peg WETH  Coinbase Wrapped BTC

Coinbase Wrapped BTC  Pudgy Penguins

Pudgy Penguins  Worldcoin

Worldcoin  THORChain

THORChain  JasmyCoin

JasmyCoin  Rocket Pool ETH

Rocket Pool ETH  FLOKI

FLOKI  Gate

Gate  GALA

GALA  Lido DAO

Lido DAO  Mantle Staked Ether

Mantle Staked Ether  Flare

Flare  Maker

Maker  Fasttoken

Fasttoken  Pyth Network

Pyth Network  Usual USD

Usual USD  NEXO

NEXO  Solv Protocol SolvBTC

Solv Protocol SolvBTC  Kaia

Kaia  KuCoin

KuCoin  Brett

Brett  Raydium

Raydium  Helium

Helium  Binance Staked SOL

Binance Staked SOL  Ethereum Name Service

Ethereum Name Service  Aerodrome Finance

Aerodrome Finance  Jupiter

Jupiter  Flow

Flow  Starknet

Starknet  Arweave

Arweave  IOTA

IOTA  Bitcoin SV

Bitcoin SV  dYdX

dYdX  Curve DAO

Curve DAO  Marinade Staked SOL

Marinade Staked SOL  Core

Core  NEO

NEO  Polygon

Polygon  Decentraland

Decentraland  Solv Protocol SolvBTC.BBN

Solv Protocol SolvBTC.BBN  ApeCoin

ApeCoin  Fartcoin

Fartcoin  Arbitrum Bridged WBTC (Arbitrum One)

Arbitrum Bridged WBTC (Arbitrum One)  ether.fi Staked ETH

ether.fi Staked ETH  Zcash

Zcash  Eigenlayer

Eigenlayer  Jito

Jito  Chiliz

Chiliz  ai16z

ai16z  Conflux

Conflux  Popcat

Popcat  Mina Protocol

Mina Protocol  L2 Standard Bridged WETH (Base)

L2 Standard Bridged WETH (Base)  Jupiter Staked SOL

Jupiter Staked SOL  USDD

USDD  Compound

Compound  Ronin

Ronin  SPX6900

SPX6900  Synthetix Network

Synthetix Network  Arbitrum Bridged WETH (Arbitrum One)

Arbitrum Bridged WETH (Arbitrum One)  Chia

Chia  dYdX

dYdX  Binance-Peg Dogecoin

Binance-Peg Dogecoin  DOG•GO•TO•THE•MOON (Runes)

DOG•GO•TO•THE•MOON (Runes)  Amp

Amp  Peanut the Squirrel

Peanut the Squirrel  Axelar

Axelar  ZKsync

ZKsync  Notcoin

Notcoin  Ether.fi Staked BTC

Ether.fi Staked BTC  LayerZero

LayerZero  Tether Gold

Tether Gold  Baby Doge Coin

Baby Doge Coin  Mantle Restaked ETH

Mantle Restaked ETH  Terra Luna Classic

Terra Luna Classic  Reserve Rights

Reserve Rights  Grass

Grass  Coinbase Wrapped Staked ETH

Coinbase Wrapped Staked ETH  Turbo

Turbo  Usual

Usual  Oasis

Oasis  Blur

Blur  cat in a dogs world

cat in a dogs world  ORDI

ORDI  Safe

Safe  1inch

1inch  Super OETH

Super OETH  Trust Wallet

Trust Wallet  Creditcoin

Creditcoin  Beldex

Beldex  Avalanche Bridged BTC (Avalanche)

Avalanche Bridged BTC (Avalanche)  sUSDS

sUSDS  APENFT

APENFT  PAX Gold

PAX Gold  Gigachad

Gigachad  pumpBTC

pumpBTC  Kusama

Kusama  Nervos Network

Nervos Network  Polygon PoS Bridged WETH (Polygon POS)

Polygon PoS Bridged WETH (Polygon POS)

Elements of the Payment Stablecoin Act have the potential to be beneficial for American consumers — but critics claim other parts are “unconstitutional.”

Republican Cynthia Lummis and Democrat Kirsten Gillibrand have become something of a bipartisan, pro-crypto double act in Congress — leading the charge in the push to offer regulatory clarity on digital assets in the U.S.

Their latest legislative effort has centered on stablecoins, with both arguing that a well-defined framework is needed to protect consumers and ensure the dollar remains dominant as digital payments continue to gain momentum.

One of the most significant proposals in the Lummis-Gillibrand Payment Stablecoin Act would see algorithmic stablecoins banned altogether in the U.S. — preventing coins that aren’t backed by real-world assets from launching. This is a clear nod to the catastrophe that surrounded Terraform Labs’ UST, which suffered a death spiral after losing its peg to the dollar in 2022.

This particular proposal has caused concern among some advocacy groups — namely Coin Center. While the nonprofit made clear it is no fan of UST, it’s argued that an outright ban on algorithmic stablecoins is “not just bad policy but unconstitutional as well.” The think tank’s executive director, Jerry Brito, argued:

“There can be ‘algorithmic stablecoins’ that (unlike Terra) are fully decentralized, with no issuers or promoters making any promises. In such cases a ban on ‘algorithmic stablecoins’ is essentially a ban on publishing code, which would violate free speech rights.”

Jerry Brito

Other areas of the Payment Stablecoin Act also raise more questions than answers. For one, it leaves the status of some digital assets, such as MakerDAO’s decentralized offering DAI, unclear, to say the least.

There could also be headaches for Circle which issues USDC — the world’s second-largest stablecoin with a market capitalization of $33 billion at the time of writing. The company is headquartered in Massachusetts, meaning it would firmly fall under the purview of the Payment Stablecoin Act. Given the proposals state that trust companies would only be able to issue up to $10 billion in stablecoins, Circle would be unable to operate in its current form without becoming a regulated depository institution.

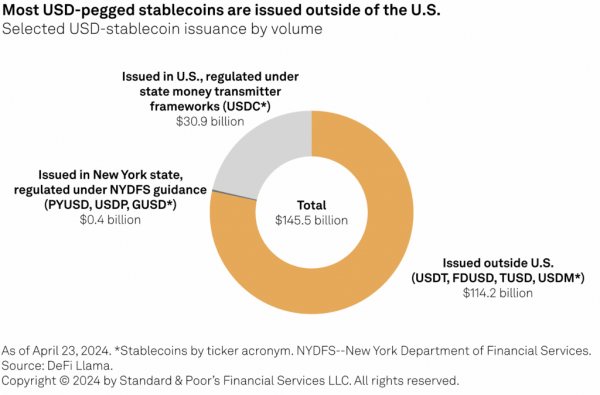

Although both politicians rightly argue that USD-denominated stablecoins based in other jurisdictions “are currently writing rules for the dollar,” it’s also unclear how any of these rules could apply to Tether. USDT dominates the industry with a market cap of $110 billion, but is based offshore. Research from S&P Global also suggests that — out of the $145 billion market for USD-pegged stablecoins — about 80% have been issued outside of the U.S.

Source: S&P Global

Promising measures

Elements of the Payment Stablecoin Act have the potential to be beneficial for American consumers.

For one, any legislation that opens the door to the mass adoption of stablecoin payments is to be welcomed. As Lummis and Gillibrand note, cross-border transactions using legacy systems can take up to 10 days to clear — and often come with punishing fees attached. By contrast, stablecoins offer near-instant settlement at much lower cost.

This could be transformative for remittances, which involve foreign workers sending funds back home to their families. Data from the World Bank suggests this sector was worth an estimated $669 billion in 2023, but the typical cost of remittances stands at 6.2%. That’s $41 billion that could have benefitted local economies — all eaten up by transaction fees.

If signed into law, these proposals would introduce safeguards to ensure all stablecoins are properly backed on a one-to-one basis with dollars held in reserve, and introduce FDIC deposit insurance in the event an issuer went bust. In the banking sector, this currently protects customers to the tune of $250,000 automatically.

Lummis and Gillibrand also argue the measures could mitigate the prospect of de-dollarization as major economies around the world work to build their own financial systems — “enshrining American values and the dollar as the base currency for the $4.5 trillion global economy.” S&P Global primary credit analysts Mohamed Damak and Andrew O’Neill went on to suggest that the bill’s approval could lead to banks issuing their own stablecoins.

The big question now is whether the Payments Stablecoin Act will pass, and how. The global law firm Akin warned:

“As the focus turns to the upcoming election and legislative activity slows, there are limited opportunities to move the bill through Congress.”

Akin

Read more: Circle, Solana team up to boost USDC interoperability

Source